|

No matter what your age group is planning for your financial security will help you to be better equipped in handling your family life. As a couple in late 20s here are a few interesting schemes you can invest in.

Insurance

This is a good time to purchase an insurance policy for you and your family. There are several plans you can opt from based on your immediate and future requirement such as health insurance, life insurance, child plan, car insurance, home insurance, motor insurance, protection plans, investment plan, retirement plan, savings plan, to name a few.

Fixed Deposit

This is a low-risk, high return investment. Simply park a lump sum amount in your FD account and earn interest starting from 8.40% on it. Interest income up to Rs. 10,000 is tax-free. While, you can submit Form 15G and Form 15H to save tax on interest income of Rs. 10,000 or more.

Public Provident Fund (PPF)

It has a longer tenor of up to 15 years so the impact of compounding of tax-free interest becomes huge especially in later years. This is a safe investment as interest earned and principal invested is backed by sovereign guarantee.

Other investments such as real estate and gold are other lucrative options you can consider. However, the kind of savings you choose depends on your financial goals both immediate and of the future. Talk to financial planners, your family and check out aggregator sites to learn more and invest wisely.

0 Comments

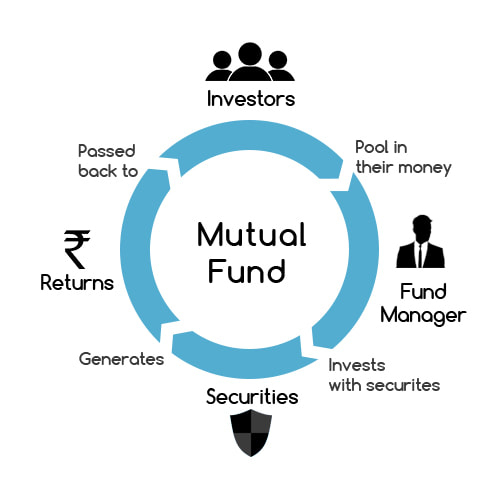

Before you pick an investment option from mutual fund and fixed deposit it is better to have a financial roadmap. This will help you better divide your funds based on immediate needs or for future. You can check aggregator sites to learn more.

Let’s look at crucial differences between mutual fund and fixed deposit to help you take an informed decision. #1 Risk Fixed deposit is a zero-risk investment as it is free from market fluctuations. It lets you earn interest on a fixed amount which you can withdraw before maturity or at maturity of the deposit. Mutual fund is subject to market fluctuations even though the investment covers a range of stocks within a fund. So, eventual gains depend on existing market conditions and hence can be fluctuating. #2 Return on Investment Fixed deposit offers an appreciable fixed interest income on the deposited amount over the specified tenure. Mutual fund income could be potentially higher or lower based on your judgement and investment in the market. Rising market results in good earnings while falling market

#3 Withdrawal

Fixed deposits will let the depositor make a premature withdrawal though there will be small charges. On withdrawal at maturity of the deposit the depositor can save tax by filling up Form 15G and Form 15H. Mutual funds will let the investor make a premature withdrawal if the minimum holding period is complete. But, there will be an exit load charge (around 1%) in this case. For so many years, you were only aware of those two to three investment options. Most of these neither give a higher return on investment nor they show you how much you are going to get in the end. Here is a list of some new investment avenues in 2018:  Cryptocurrency- Recently, this market is growing at an exponential rate, and more and more people are getting interested in investing in cryptocurrencies like Bitcoin and Ethereum. Cryptocurrency works on blockchain technology, so it secured, and it gives you the opportunity to become rich on daily basis.  Fixed Deposit- FD is the safest mode of investment, where you are assured to get a higher return on investment as the rate of interest is very high as compared to interest earned from any savings account. You can easily check and calculate the exact maturity amount of the FD by using Fixed Deposit interest calculator and remain assured that you are definitely going to get this amount after maturity.  Gold- It is considered to be the most robust form of investment. In 2018, many new forms of investments have evolved like Gold ETFs and Gold mutual funds within the category of gold investments.  Mutual Funds- The best way to start investing in mutual funds is through Systematic Investment Plans or SIP. Here you can invest a fixed sum either monthly or quarterly for a specific duration and later you may get the money along with the interest.  To know about the other options, read: http://whazzup-u.com/profiles/blogs/plan-to-save-in-2018-refer-to-these-new-age-investment-options

At the beginning of every financial year, almost all corporate employee has to fill an investment declaration form, declaring his investment plan for the year. Though it becomes annoying sometimes, if you take my words - it is no less than being gifted by your loved ones on valentines. When your employer asks you to declare your investment plan, he/she never intends to discomfort you with the burden. They do so to help you save your hard earned money from being consumed by the Income-tax department. The same help them accurately file your income tax and to ensure you end up with a higher in-hand salary. Therefore, rather than avoiding the declaration, proactively shoulder on the responsibility. But before you declare your investment plan for FY 2018-19, keep these things in mind.

Lastly, while filling the declaration form, ensure minimum chances of errors. Fill the form properly and manage an efficient investment plan declaration. |

CATEGORY

About Author:Aman is working in the domain of Investment management in one of the top universities. He has published research papers and case studies in Investment and Fixed Deposit marketplace. He is an avid blogger in the domain of Investment management. you can also find him on social networking platforms. Archives

August 2022

|

RSS Feed

RSS Feed