|

When you consider all the other investments available in the market, FD is one of the safest ones around. You create a deposit for a fixed amount of time and earn interest on it. Only if you break the FD in case of an emergency will a penalty charge be levied, else, the FD will remain safe as well as earn a steady rate of interest as per your policy. Although it is normal to worry with regards to an FD investment, the only time you will have to worry about your FD investment not being safe is if your bank or lender is unstable or is headed towards insolvency. Why FDs are the best investment options:

There are many other factors which affect the safety of your FD investment, especially if the amount is greater than one lakhs.

2 Comments

Have you ever thought of your life post retirement? It is very important to save for your retirement so that you do not regret. In this age of high inflation being retired is not easy at all. Nobody wants to be hard pressed for funds once they retire. That is the only reason to focus on planning ahead so that you can have a comfortable life along with your family after you retire at the age of 60 years or so. A pension is an amount paid by your government and employer periodically when you retire. On the contrary, a provident fund is one in which both you and your employer contribute throughout your work tenure. Your provident fund is paid back to you in lump sum when you retire or leave your organization. However, a gratuity is an incentive scheme offered to you if you stayed with a company for at least 5 years or more.  Have a look about the Investment ideas for your surplus fund Once you retire and after you have received all your various amounts you were entitled to, it becomes your responsibility to make sure that the funds you gain last as long as possible. Thus, it becomes necessary to plan ahead. While analyzing options, you can target lower risk, regular income generating options. here is a list of such options:

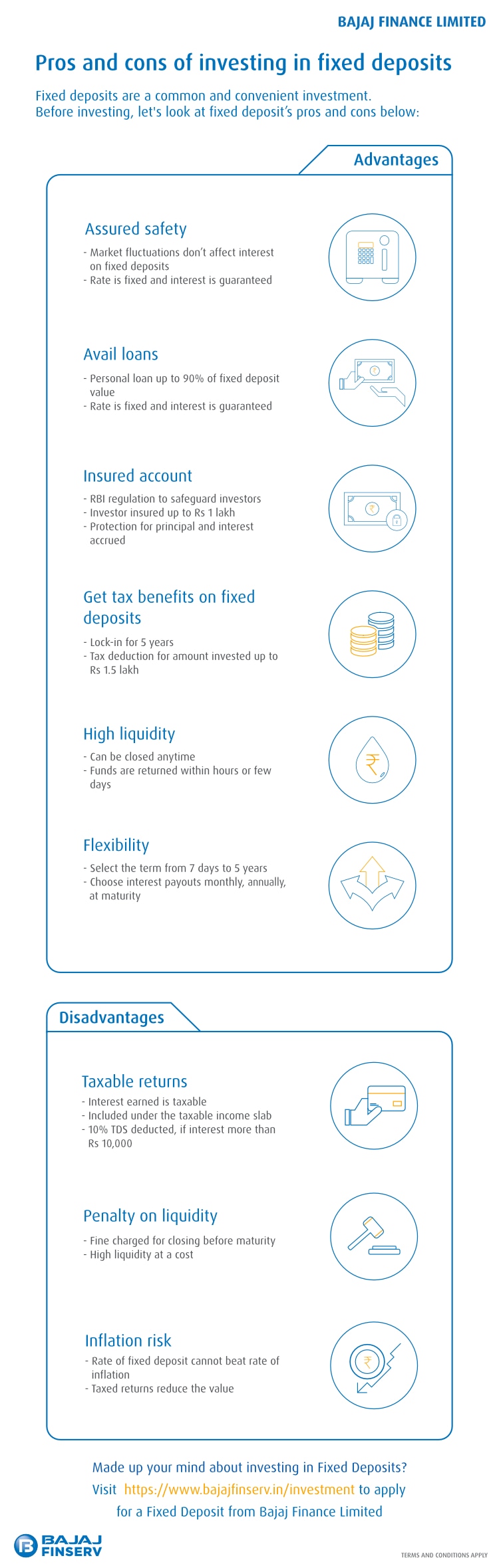

It goes without saying that managing liquidity and the assets is a crucial aspect of the personal financial planning. But it is often seen that those with handsome business portfolios find it tough to tackle liquidity of funds. You never know when a sudden need of cash can compel you to a situation where you see that there is no other way than to sell off your assets in exchange for an amount which is lower than the actual value. Fortunately, enough, the traditional bank deposits can come to your rescue at those difficult moments.  Reaping the Benefits of Fixed Deposits There are numerous banks and notable NBFCs that offer fixed deposits and allow to take a personal loan against FD. You can raise money in a small amount of time without breaking the Fixed Deposit. Lowered Rate of Interest: One benefit of taking a personal loan against fixed deposit is that you can enjoy a lower rate of fixed deposit than regular personal loans. You can get a loan by paying 1% higher than the rate from Fixed Deposit. This saves a lot of money which you can use to pay interest on the loan. Easy to Obtain: It’s pretty simple to get a personal loan from Fixed Deposit. It generally takes less than a day. You’ll just have to submit the application form and some necessary documents like identity proof and certificate of deposit. No Prepayment Penalty: You won’t have to pay any penalty charges if you want to prepay the personal loan amount before the specified date. The lending authority can charge a small processing fee, but you can get some banks that waive it. Overdraft Facility: This facility against Fixed Deposit lets borrowers access liquidity. You can access the funds for some time and repay before its time. You’ll continue to receive the benefits of the Fixed Deposit while managing expenses with the loan against the deposit. Manage Cash Crunch: Ever since demonetization in November, the economic situation hasn’t been stable. The cash crunch is still present. In this situation, if you take personal credit from your deposit, you can manage any urgent expenses effortlessly. If you take a personal loan against a Fixed Deposit, you should look for ways to raise short term money. That’s because if you fail to repay the loan on time, you may end up losing the deposit since the bank would foreclose it to repay the money you’ve lent. That affects the CIBIL report. So, you should make sure to raise your funds to pay back the loan amount in time. Taking out a personal loan on your Fixed Deposit is one of the best choices that you can make when it comes to maintaining your deposit and still taking out the loan you need. Tips of Alternative options to FD Withdrawal Fixed Deposits are the default investment option for most people looking to invest their money. Even in this age the Fixed Deposit is still the most popular investment venture in India. But they’re not as all-round amazing as they seem. They do have little niggles that you should be worried about. So, should you still invest in fixed deposits? The Advantages and Disadvantage of Fixed Deposits Fixed deposits: Advantages, FD interest calculation & tax benefits Pros: Security of Principal: The amount you invest in bank or NBFC FDs are secure. These deposit schemes are governed by RBI regulations, so the investments are safe. Bank deposits upto Rs.1 lakh per customer per bank is insured. This makes FD is one of the safest methods of investing that you can have. Assured Returns The interest rate on FD is fixed at the time of opening the deposit. Provided you don’t close the FD before maturity, the promised maturity amount will be paid to you. This includes the principal and the accrued interest. Cons: Low Return on Investment Interest rates on FDs are low. The amount invested won’t grow enough to make up for inflation rates over time. Taxes The interest earnings on all FDs are taxed according to your tax slab. Banks will do a TDS on interest earnings above Rs.10,000 in a year. But, all of your interest earnings on each FD is taxable, even if it is below Rs.10,000. |

CATEGORY

About Author:Aman is working in the domain of Investment management in one of the top universities. He has published research papers and case studies in Investment and Fixed Deposit marketplace. He is an avid blogger in the domain of Investment management. you can also find him on social networking platforms. Archives

August 2022

|

RSS Feed

RSS Feed